- Understanding the Basics of Leveraged Buyouts

- Benefits of Using an LBO Model

- Components of an LBO Model

- LBO Model Valuation Techniques

- How to Assess LBO Model Sensitivity and Risk Analysis?

- LBO Model Key Metrics and Outputs

- Best Practices for Building and Using an LBO Model

- Example: How to Build an LBO Model for a Sample Transaction?

- Conclusion

Whether you’re a finance professional, an aspiring investor, or simply someone interested in understanding LBO transactions, this guide will provide you with a comprehensive overview and step-by-step instructions on how to build and utilize an LBO model effectively.

Understanding the Basics of Leveraged Buyouts

LBO transactions are a popular strategy used in corporate finance for acquiring companies. Let’s start by understanding the fundamentals of LBOs, the key parties involved, and the benefits and risks associated with these transactions.

What is a Leveraged Buyout (LBO)?

A Leveraged Buyout, or LBO, refers to the acquisition of a company using a significant amount of borrowed funds. In an LBO transaction, a financial sponsor or private equity firm acquires a target company, typically using a combination of equity and debt. The acquired company’s cash flow and assets are then used to repay the debt over time.

Key Parties Involved in an LBO Transaction

An LBO transaction involves several key parties, each playing a crucial role:

- Financial Sponsor/Private Equity Firm: The entity that initiates and funds the acquisition, typically using a combination of its own capital and external financing.

- Target Company: The company being acquired in the LBO transaction.

- Management Team: The individuals responsible for overseeing the operations and strategic direction of the target company post-acquisition.

- Lenders: Financial institutions or investors providing the debt financing for the LBO.

- Investors: Individuals or institutions investing in the equity of the acquiring entity (financial sponsor), often including the financial sponsor’s own capital and funds from limited partners.

- Advisory Professionals: Legal, financial, and accounting experts who provide guidance and support throughout the LBO process.

Leveraged Buyouts Benefits and Risks

Leveraged buyouts offer various benefits and opportunities for both the financial sponsor and the target company. However, they also come with certain risks that need to be carefully assessed and managed. Here are some key benefits and risks of LBO transactions:

LBO Model Benefits:

- Enhanced Returns: LBOs provide an opportunity for financial sponsors to generate attractive returns by using leverage to amplify equity returns.

- Operational Improvements: LBOs often involve restructuring and optimizing the target company’s operations, which can lead to increased efficiency and profitability.

- Alignment of Interests: LBOs align the interests of management and financial sponsors, as both parties have a financial stake in the success of the acquired company.

- Opportunity for Growth: LBOs can provide the target company with the necessary capital and resources to pursue growth strategies, such as acquisitions or geographic expansion.

LBO Model Risks:

- Financial Risk: LBOs involve significant debt, which increases the financial risk for both the acquiring entity and the target company.

- Market and Economic Risk: LBOs are susceptible to changes in market conditions and economic downturns, which can impact the performance and valuation of the acquired company.

- Operational Challenges: The process of integrating and managing an acquired company can present operational challenges, such as cultural differences and conflicting management styles.

- Exit Strategy Risk: The success of an LBO transaction depends on the ability to exit the investment at an attractive valuation, which can be affected by market conditions and investor appetite.

Benefits of Using an LBO Model

Before diving into the components and mechanics of an LBO model, it’s important to understand why these models are valuable tools for analyzing and evaluating potential LBO transactions.

Assessing the Feasibility of an LBO Transaction

LBO models allow you to assess the financial feasibility of an LBO transaction by projecting the future financial performance of the target company and analyzing the potential returns for the financial sponsor. With an LBO model, you can:

- Evaluate the target company’s historical financials and industry trends.

- Make assumptions about future revenue growth, operating expenses, and capital expenditures.

- Calculate key financial metrics, such as EBITDA, net income, and cash flows, to assess the potential profitability and cash generation of the target company.

- Determine the optimal debt and equity mix to fund the acquisition.

Evaluating Potential Returns for Investors

LBO models enable you to estimate the potential returns for investors by calculating key performance metrics and conducting sensitivity and scenario analysis. With an LBO model, you can:

- Calculate financial metrics such as cash-on-cash (CoC) multiple, internal rate of return (IRR), and return on investment (ROI).

- Assess the impact of different exit strategies and exit multiples on investor returns.

- Conduct scenario analysis to understand how changes in key assumptions, such as revenue growth or interest rates, affect the financial performance and returns of the LBO investment.

Analyzing the Impact of Leverage on Cash Flows and Financial Metrics

One of the defining features of an LBO transaction is the use of leverage. LBO models allow you to analyze the impact of leverage on the cash flows and financial metrics of the acquired company. With an LBO model, you can:

- Calculate the interest expense and principal repayments associated with the debt financing.

- Evaluate the debt service coverage and debt capacity of the target company.

- Assess the financial flexibility and ability to generate sufficient cash flows to meet debt obligations.

- Understand the implications of different debt structures and interest rates on the financial viability of the LBO transaction.

Components of an LBO Model

An LBO model consists of multiple interconnected components that together form a comprehensive financial analysis framework.

Gathering Historical Financial Data

The first step in building an LBO model is gathering the historical financial data of the target company. This data will serve as the foundation for your projections and analysis. Obtain the following financial statements for the past few years:

- Income Statement: Provides information on the company’s revenues, expenses, and profitability.

- Balance Sheet: Presents the company’s assets, liabilities, and shareholders’ equity at a specific point in time.

- Cash Flow Statement: Details the company’s cash inflows and outflows from operating, investing, and financing activities.

Building Revenue Projections

Revenue projections are a crucial aspect of an LBO model, as they drive the financial performance of the target company. When building revenue projections:

- Analyze historical revenue trends and consider external factors impacting the industry.

- Make assumptions regarding future revenue growth based on market research and the target company’s competitive position.

- Incorporate seasonality or cyclical patterns, if applicable.

- Break down revenue by product lines, customer segments, or geographic regions, if necessary.

To calculate projected revenue, use the following formula:

Projected Revenue = Historical Revenue x (1 + Revenue Growth Rate)

Estimating Expenses and Operating Costs

Accurate estimation of expenses and operating costs is essential for building a realistic LBO model. When estimating expenses:

- Analyze historical expense ratios and trends.

- Identify cost-saving opportunities and operational efficiencies that could be realized post-acquisition.

- Make assumptions about inflation rates and changes in input costs.

- Consider any non-recurring expenses that may impact future financials.

Estimate operating costs using the following formula:

Operating Costs = Revenue x Operating Cost Ratio

Determining Financing Structure and Interest Rates

The financing structure and interest rates significantly impact the cash flow and returns of an LBO investment. When determining the financing structure:

- Assess the optimal mix of debt and equity based on the financial sponsor’s risk appetite and return expectations.

- Evaluate different sources of debt financing, such as senior debt, mezzanine debt, and high-yield bonds.

- Negotiate favorable terms and conditions with lenders to secure the best possible interest rates and repayment schedules.

Creating Debt Schedules and Repayment Plans

Debt schedules outline the repayment of principal and interest over the life of the debt. When creating debt schedules:

- Incorporate the different debt tranches, interest rates, and maturities into the model.

- Calculate the annual principal repayments based on the agreed-upon repayment plan.

- Calculate the interest expense using the average outstanding debt balance and the applicable interest rates.

The formula for calculating interest expense is as follows:

Interest Expense = Average Debt Balance x Interest Rate

Incorporating Tax Considerations

Tax implications play a significant role in the financial analysis of LBO transactions. When incorporating tax considerations:

- Understand the target company’s tax obligations and applicable tax rates.

- Consider any tax benefits or deductions resulting from debt financing or other transaction-related expenses.

- Incorporate tax provisions, such as deferred tax assets and liabilities, into the model.

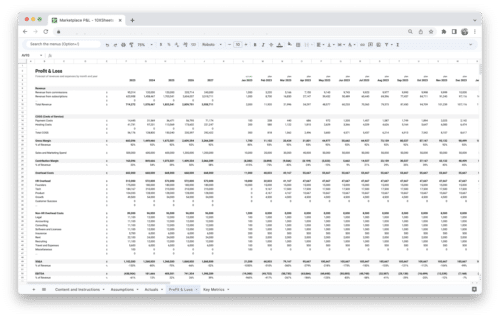

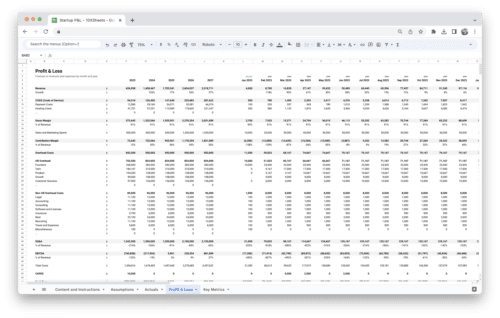

Calculating Cash Flows and Valuations

Cash flows and valuations are critical outputs of an LBO model and serve as the basis for evaluating the financial performance and potential returns of the investment. Calculate the following cash flows:

- Operating Cash Flow: Cash generated from the target company’s core operations.

- Investing Cash Flow: Cash flows associated with capital expenditures and other investments.

- Financing Cash Flow: Cash flows resulting from debt repayments, equity injections, and dividends.

Analyzing Sensitivity and Risk Factors

LBO models should incorporate sensitivity and risk analysis to assess the impact of changing key assumptions on the financial performance and returns of the investment. Consider the following factors:

- Interest Rates: Evaluate the sensitivity of cash flows and profitability to changes in interest rates.

- Revenue Growth: Assess how variations in revenue growth rates affect the financial viability of the transaction.

- Exit Multiples: Analyze the potential impact of different exit multiples on the overall returns of the investment.

- Other Risk Factors: Incorporate risk factors specific to the industry, market conditions, or the target company itself.

LBO Model Valuation Techniques

Valuation is a critical aspect of LBO modeling and helps determine the fair value of the target company and the potential returns for the financial sponsor.

Enterprise Value (EV) and Equity Value

Enterprise Value (EV) represents the total value of a company, including its debt and equity. Equity Value represents the value attributable to the shareholders. Calculate these values using the following formulas:

- Enterprise Value (EV): EV = Total Debt + Equity Value

- Equity Value: Equity Value = EV – Total Debt

Multiple-Based Valuation

Multiple-based valuation involves comparing the target company’s financial metrics to those of similar companies in the industry. Common multiples used in LBO models include:

- Enterprise Value to EBITDA (EV/EBITDA): EV/EBITDA = Enterprise Value / EBITDA

- Price to Earnings (P/E) Ratio: P/E Ratio = Stock Price / Earnings per Share (EPS)

Discounted Cash Flow (DCF) Analysis

DCF analysis estimates the present value of future cash flows generated by the target company. The DCF formula is as follows:

DCF = [CF1 / (1+r)^1] + [CF2 / (1+r)^2] + … + [CFn / (1+r)^n]

Where:

- CF1, CF2, …, CFn: Projected cash flows for each period.

- r: Discount rate representing the required rate of return.

Comparable Company Analysis

Comparable Company Analysis involves comparing the target company’s financial metrics to those of similar publicly traded companies. Key steps in performing a Comparable Company Analysis include:

- Selecting a group of comparable companies in the same industry.

- Calculating relevant financial ratios, such as Price/Earnings (P/E), Price/Sales (P/S), and Price/Book (P/B).

- Determining a valuation range based on the observed multiples of the comparable companies.

How to Assess LBO Model Sensitivity and Risk Analysis?

LBO models involve numerous assumptions, and it’s crucial to assess the sensitivity of these assumptions to better understand the potential risks and returns of the investment.

Identifying Key Assumptions

Identify the key assumptions used in your LBO model, such as revenue growth rates, operating margins, interest rates, and exit multiples. These assumptions have a significant impact on the model’s outputs and should be analyzed for sensitivity.

Performing Scenario Analysis

Scenario analysis involves assessing the impact of different scenarios on the financial performance and returns of the LBO investment.

- Base Case: Reflects your best estimate of the target company’s future performance based on the assumptions.

- Upside Case: Represents a more optimistic scenario with higher revenue growth rates or improved operating margins.

- Downside Case: Represents a more pessimistic scenario with lower revenue growth rates or decreased operating margins.

Sensitivity Analysis for Key Assumptions

Sensitivity analysis involves analyzing how changes in key assumptions affect the financial metrics and returns of the LBO investment. Focus on the following key factors:

- Interest Rates: Assess the impact of changes in interest rates on debt service costs and cash flows.

- Revenue Growth: Analyze how variations in revenue growth rates affect the company’s profitability and investor returns.

- Exit Multiples: Evaluate the sensitivity of equity value and investor returns to changes in exit multiples.

Incorporating Risk Factors into the LBO Model

Incorporate risk factors specific to the target company, industry, and market conditions into your LBO model. Consider the following risk factors:

- Macroeconomic Risks: Evaluate the impact of economic downturns, inflation, or geopolitical events on the target company’s performance.

- Industry Risks: Analyze risks related to industry competition, technological disruptions, regulatory changes, and market trends.

- Company-Specific Risks: Assess risks associated with the target company’s competitive position, management team, and operational vulnerabilities.

LBO Model Key Metrics and Outputs

LBO models produce various key metrics and outputs that help assess the financial performance and potential returns of the investment.

Cash-on-Cash (CoC) Multiple

The Cash-on-Cash (CoC) multiple represents the ratio of the total cash flow distributed to equity investors over the life of the investment to the total equity invested. It measures the return on investment for the equity investors. Calculate the CoC multiple using the following formula:

CoC Multiple = Total Cash Flow to Equity / Total Equity Invested

Internal Rate of Return (IRR)

The Internal Rate of Return (IRR) is the discount rate that equates the present value of cash inflows and outflows from an investment. It represents the annualized return generated by the investment. Calculate the IRR using iterative techniques or financial software.

Return on Investment (ROI)

Return on Investment (ROI) measures the profitability of an investment by comparing the gain or loss generated relative to the amount invested. Calculate the ROI using the following formula:

ROI = (Net Profit – Initial Investment) / Initial Investment

Debt-to-Equity Ratio

The Debt-to-Equity ratio compares the amount of debt financing to the equity investment in an LBO transaction. It provides insights into the financial leverage employed in the transaction. Calculate the Debt-to-Equity ratio using the following formula:

Debt-to-Equity Ratio = Total Debt / Total Equity

Payback Period

The Payback Period measures the time required to recoup the initial investment in an LBO transaction through cash flows. It helps assess the speed at which the investment generates returns. Calculate the Payback Period by determining the point at which cumulative cash flows equal the initial investment.

Exit Strategies and Exit Multiples

Exit strategies and exit multiples play a crucial role in determining the potential returns and exit options for an LBO investment.

- IPO (Initial Public Offering): Taking the target company public through an IPO, enabling the financial sponsor to sell its shares in the public markets.

- Trade Sale: Selling the target company to a strategic buyer in the industry.

- Secondary Buyout: Selling the target company to another private equity firm.

- Dividend Recapitalization: Distributing cash to equity investors by recapitalizing the company with additional debt.

Evaluate potential exit multiples by analyzing historical multiples for comparable companies and considering market conditions.

Best Practices for Building and Using an LBO Model

Building an LBO model requires attention to detail and adherence to best practices. Follow these guidelines to create an effective and robust LBO model:

Data Sources and Gathering Relevant Information

- Gather reliable and up-to-date financial statements and other relevant information from reputable sources.

- Verify the accuracy of the data and cross-reference multiple sources when available.

- Use industry reports, market research, and expert opinions to inform your assumptions and projections.

Financial Modeling Techniques and Excel Tips

- Familiarize yourself with financial modeling best practices, such as clear organization, consistency, and formula integrity.

- Utilize Excel’s built-in functions, formulas, and data analysis tools to streamline your modeling process.

- Use appropriate formatting, color coding, and data validation techniques to enhance the clarity and usability of your model.

Sensible Assumptions and Scenario Planning

- Ensure that your assumptions are reasonable, well-documented, and supported by market research or historical data.

- Consider a range of scenarios and sensitivities to capture the potential outcomes and risks associated with the investment.

- Document your assumptions, scenario analyses, and the rationale behind key decisions to enhance transparency and auditability.

Documentation and Model Auditability

- Maintain clear and organized documentation throughout the model-building process.

- Label all inputs, formulas, and assumptions clearly to facilitate model navigation and review.

- Include an assumptions log that provides a comprehensive overview of all inputs and the sources of information.

Periodic Model Review and Updates

- Regularly review and update your LBO model to reflect changes in market conditions, industry trends, and company-specific factors.

- Validate and stress-test your model against historical data or actual outcomes to improve accuracy and reliability.

- Incorporate feedback from colleagues, mentors, or subject matter experts to refine your model and ensure its quality.

Example: How to Build an LBO Model for a Sample Transaction?

Let’s look at a detailed case study that demonstrates the step-by-step process of building an LBO model for a sample transaction. By following along with the case study, you’ll gain a practical understanding of how to apply the concepts and techniques discussed in the guide.

- Gather Historical Financial Data: Collect the historical financial statements (income statement, balance sheet, and cash flow statement) for the target company.

- Analyze Historical Performance: Review the historical financials and identify trends, growth rates, and key performance metrics.

- Identify Acquisition Assumptions: Determine the acquisition price, financing structure, and key assumptions such as revenue growth rates and operating margins.

- Build Revenue Projections: Use historical growth rates, market research, and other factors to estimate future revenue growth.

- Estimate Operating Costs: Analyze historical expense ratios and apply assumptions to estimate future operating costs.

- Incorporate Debt Financing: Determine the debt structure, interest rates, and repayment schedules based on negotiations with lenders.

- Calculate Cash Flows and Financial Metrics: Build the cash flow statement, calculate EBITDA, interest expense, and other financial metrics.

- Perform Sensitivity and Scenario Analysis: Assess the impact of changes in key assumptions on the financial performance and returns of the investment.

- Conduct Valuation Analysis: Use multiple-based valuation, DCF analysis, and comparable company analysis to estimate the fair value of the target company.

- Evaluate Key Metrics and Outputs: Calculate metrics such as CoC multiple, IRR, ROI, and assess the financial viability and attractiveness of the investment.

- Prepare Presentations and Reports: Summarize the analysis, findings, and recommendations in a clear and concise format for stakeholders.

By following these steps and adapting them to your specific LBO transaction, you’ll be able to build a comprehensive LBO model that provides valuable insights for decision-making.

Conclusion

Throughout this guide, we’ve explored the fundamental concepts, components, and techniques involved in building and utilizing LBO models. By now, you should have a solid understanding of LBO transactions, the benefits of LBO models, and how to create a robust LBO model from scratch.

Remember, building an effective LBO model requires attention to detail, realistic assumptions, and thorough analysis. Continuously update and refine your model as new information becomes available, and validate your assumptions against real-world outcomes to enhance its accuracy and reliability.

LBO models are powerful tools that can provide valuable insights into the financial viability and potential returns of investment opportunities. Whether you’re evaluating potential acquisitions, analyzing investment opportunities, or conducting due diligence, the knowledge and skills gained from this guide will serve you well.

Get Started With a Prebuilt Template!

Looking to streamline your business financial modeling process with a prebuilt customizable template? Say goodbye to the hassle of building a financial model from scratch and get started right away with one of our premium templates.

- Save time with no need to create a financial model from scratch.

- Reduce errors with prebuilt formulas and calculations.

- Customize to your needs by adding/deleting sections and adjusting formulas.

- Automatically calculate key metrics for valuable insights.

- Make informed decisions about your strategy and goals with a clear picture of your business performance and financial health.